Many families with children resort to housing loans to purchase an apartment. As a result of the transaction, the parents become the owners of the square meters, and the object itself becomes collateral. But not all borrowers think about how the mortgage and the child’s share are connected.

There are cases when allocating shares to children is the only chance to purchase real estate using bank funds and comply with legal requirements. For example, when funds from a family certificate were used to obtain or partially repay a loan.

In this article we will look at how to do this before and after repayment of the mortgage, and we will understand the nuances and subtleties of the procedure.

Difficulties in allocating a child's share

The rights of minors are enshrined in the Family Code. Their protection and monitoring of compliance are monitored by guardianship authorities. A third party, the lender, takes part in the procedure for purchasing real estate using borrowed resources. Thus, the interests of the family, the bank and the supervisory authorities must be taken into account. In this case, you must comply with current legislation. It is this composition of stakeholders that makes such transactions difficult to carry out, requiring increased attention and additional knowledge.

Is it possible to allocate a share to children?

Based on current legislation, parents must ensure the right of minors to own property. In the case of a mortgage, the allocation of a share usually occurs after all obligations have been repaid. If a family certificate was used to make the first payment or early repayment, allocating a share to the child is not only possible, but absolutely necessary.

Let's consider another situation. The family plans to sell the apartment in which the minor is registered, in order to subsequently buy a new one, partially using loan funds.

In this case, permission from the guardianship to conduct the transaction will be required.

To obtain it, it is necessary to inform the supervisory authority that the child will be granted the right to own real estate, which will be purchased subsequently.

Important! It is necessary to take into account the area in the new apartment that will be available for the child. It shouldn't get smaller.

If the child is over 14 years old, his written consent to complete the transaction will be required. Here you can learn more about the nuances of the process.

The transfer of part of the property is formalized in one of these ways:

- Registration of a donation, certified by a notary. Here is more detail about this procedure.

- An agreement to transfer part of an object into the ownership of a minor. This document is also subject to notarization.

To avoid problems with subsequent registration of property rights, you should entrust the preparation of these documents to professional lawyers. You can get a free consultation on our portal.

Despite the fact that the minimum size of children's property is not established by law, in order to avoid problems with regulatory authorities, it is best to proceed from the norm - 12 square meters for each of the children.

When is an obligation to allocate shares required?

A commitment is a legally certified document. According to it, the future owner of the apartment undertakes to share the right to own housing with children and a second spouse, if any. In simple words, the obligation allows you to delay the moment of allocating children the meters they are entitled to, but obliges them to do this in the future.

This document is required to be drawn up when using the par value of maternity capital to pay part of the cost of purchasing an apartment, including a mortgage. Without it, the pension fund will not direct the money to its intended purpose. If housing is purchased in a new building under a shared participation agreement, then it is necessary to allocate shares to children after signing the act of receiving housing, before registering the property.

All cases when it is necessary to formalize an obligation:

- The property was purchased using borrowed funds; it is possible to allocate shares to children after the mortgage is paid off.

- Parents are the owners of the apartment, while the size of the property of minors has not yet been determined.

- Contributions to the cooperative continue.

- Construction of a private house is underway.

Important! From the moment of termination of obligations to third parties or receipt of documents for a built private house, the family is given six months to fulfill the intentions specified in the obligation.

Which banks provide a child with a share of the mortgage?

Before moving on to specific credit institutions, let’s figure out why not all banks are willing to allocate children’s shares until the final payment of the mortgage. The fact is that, according to current regulations protecting the rights of minors, it will be almost impossible to forcibly sell such an apartment.

If the borrower fails to meet the mortgage payment obligations on time, the lender will not be able to foreclose on the apartment partially owned by minors.

If the bank categorically refuses to allocate the child’s share until repayment, and the guardianship and trusteeship authorities do not have enough commitment, you can use the following ways out of this situation:

- Choose a mortgage program, the terms of which provide for the pledge of not purchased, but already existing real estate. Such programs have a higher rate.

- Secure children's shares in other real estate. In this case, the borrower must own another residential property or an agreement can be reached with relatives.

- Try to eliminate the claims of the guardianship authorities, obtain their consent on the basis of a notarial obligation.

- Use another bank for help.

Important! The law does not regulate exactly what part of the property can be transferred to a minor. It could be even 1/100000.

The bank’s decision on the possibility of allocating a child’s share in a mortgage may be influenced by confirmation of solvency, savings, alternative real estate or car.

Today, deals with the allocation of a children's share are concluded by Sberbank, VTB, DOM.RF (AHML).

Allocating a share to children before repaying the mortgage

As mentioned above, not all banks are ready to go through this procedure. However, large credit organizations are trying to comply with the instructions of the guardianship authorities and take the client’s side in this matter. The shares of minor family members must be determined before receiving a housing loan. Let's consider step by step how to allocate parts of property in this situation.

Peculiarities

The nuances of this procedure include:

- The need to obtain approval from the bank and guardianship authorities.

- If the funds from the maternal certificate were used for the construction of a residential building, then the share should include part of the land on which this construction is being carried out.

- When the property being purchased is under construction, registration of part of the ownership in the name of children is possible only after its completion. This occurs after the house is put into operation and the act of receiving the property is signed, but before the borrower’s ownership rights are registered.

- The need to separate the children's part must be stated in the purchase and sale agreement.

Documentation

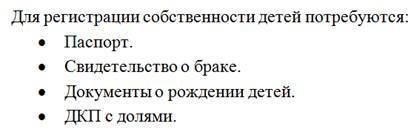

You will need to prepare:

- Identity documents.

- Apartment assessment report.

- Title documents (extract from the unified register).

- Consent of the other spouse.

- A written application to the bank about the possibility of distributing property to minors.

Procedure

The process consists of the following steps:

- Obtain a bank decision on the possibility of issuing a mortgage. At this stage, it is worth verbally discussing the possibility of allocating a child’s share and using a family certificate.

- Find an apartment.

- Obtain consent from the bank for the transaction with the allocation of a share.

- Submit a request to the guardianship authorities for approval of the transaction.

- Sign the apartment purchase agreement. The text must contain a clause on granting minors shares in the acquired property.

- Submit all documents for registration.

- Wait until state registration is completed, get a mortgage, and finally pay the seller.

Allocating a share to children after paying off the mortgage

Allocating shares to children after paying off the mortgage is much easier, because this procedure does not require additional approvals from the bank. Let's take a closer look at this process.

Peculiarities

This procedure also has a number of nuances:

- If during the term of the loan agreement another child appears in the family, he must be given a share on an equal basis with the older children.

- 6 months are allotted for collecting all documents and carrying out the transfer procedure after settlement of the loan. If the family does not have time to complete the process during this period, the supervisory authorities have the right to legally recover the nominal value of the capital back.

- To transfer ownership rights, you can draw up a gift agreement or an agreement on the transfer of part of the apartment. Both of these documents are notarized. They imply the transfer of ownership without making additional payments.

- If both spouses are owners, but the share of each of them is not determined, first it is necessary to allocate their parts, then the children's parts. It will not be possible to allocate everyone’s shares at the same time due to different reasons for receiving. Parts of the spouses are allocated on the basis of an agreement on the division of marital property, while the children are transferred by gift or agreement on the allocation of shares.

Documentation

The following kit will be required. To remove the encumbrance after paying off the mortgage:

- Mortgage from a bank.

- An application for withdrawal will be drawn up by an MFC employee. There is no need to prepare anything in advance; there is also no state duty.

Next, to divide shares in the MFC, you need to prepare:

Procedure

The mechanism for delimiting rights to property upon completion of mortgage payments is significantly simplified and does not require additional decisions from regulatory authorities or a credit institution.

Consists of the following steps:

- Receipt of a mortgage from the bank after full repayment of the mortgage loan. The bank has two weeks from the date of the last payment to issue it.

- Registration of removal of encumbrance. The set is transferred to the MFC, then the owner receives a new paper from the unified register without information about the mortgage. We wrote in detail about this procedure earlier. You will need a certificate confirming the closure of the mortgage and the absence of debt to the bank.

- Drawing up and notarization of the basis for the division of property (agreement on the voluntary transfer of part of the property, gift agreement).

- Transfer of documentation to the registration authority. The application is submitted by each participant on his own behalf (parents act for minors), the form is filled out by MFC employees.

Let us summarize based on all the above information. It is possible to differentiate children's shares before and after repayment of the mortgage. To avoid disagreements with supervisory authorities, shares that are comparable to the nominal value of the capital should be transferred.

You should carefully select a lender; preference should be given to those banks that do not interfere with the transfer of the part of property due to minors.

It is best to prepare documents for the transfer of shares from a specialist in this field.

Dear readers! The situation in the mortgage market is changing very quickly. The article describes the general rules. To resolve your individual situation, contact our online specialist lawyer.

Was it useful and interesting? Like or share the post on social networks. The duty lawyer of our portal is always happy to answer your questions.

Read further the article about the agreement on the allocation of shares.

Does Sberbank allocate shares to children on a mortgage?

If Sberbank allocates shares to children, then why is there a lot of information on the Internet that it is impossible to formalize this? The problem arises for those people who want to provide their child with guaranteed housing before repaying their housing loan. Few people understand how possible this is. And even fewer parents have enough legal knowledge to carry out the procedure correctly. Therefore, let's talk about everything in order in simple words.

Is it possible to allocate shares to children in a mortgaged apartment?

According to statistics, about a third of families use mortgage loans when purchasing housing. Two- and three-room apartments in new buildings are popular among the population. In such houses, the rooms have sufficient area so that each family member has the required number of square meters for a comfortable stay.

A mortgage in Sberbank involves providing a share to a child if the parents have used maternity capital, which is 453,026.00 rubles.

We remind you that money is paid to families upon the birth of their second baby. The procedure involves formalizing an obligation to allocate a share.

The document is long-term, and people become actual owners after repaying the debt to Sberbank.

You can allocate a share to a child if the guardianship authorities require it. In this case, there is no need to use maternal capital as a down payment.

Guardianship authorities require parents to register a share in advance. The bottom line is that if the debt to Sberbank is not repaid and the apartment is repossessed, then at the time of its sale the interests of the baby will be protected.

But such deals come with a number of difficulties.

Possible difficulties

Allocating shares to children adds to the problems. Mortgage lending is a complex procedure, given the mass of documents and aspects that Sberbank takes into account when determining the terms of the loan. The controversial points are:

- The use of maternity capital does not necessarily imply a share of real estate for the child.

- The decision to sell real estate obliges parents to obtain Sberbank approval for the transaction.

- The share does not have to be the same as in the previous apartment. When applying for a mortgage, it may decrease.

- The presence of a share does not deprive Sberbank of the right to evict the father and mother in the event of debt on the loan.

When registering a share, they receive the approval of Sberbank. To increase your chances, do the following:

- carefully choose a lender (Sberbank is considered the best option);

- improve (if necessary) credit history, eliminate all debts to banks;

- provide Sberbank with collateral in the form of other property owned by the applicant;

- distribute children's shares in other apartments and houses of second-degree relatives (grandparents, aunts, uncles).

In this case, you can count on a favorable distribution of shares and guaranteed approval of Sberbank. So, if parents live in a house or apartment with their grandmother and receive living space as an inheritance, it can be mortgaged. Then the share can be redistributed so that in the new apartment taken on a mortgage, the child is entitled to a ¼ share.

Until the debt to Sberbank is repaid, the collateral property is pledged as a guarantee. After repayment, both objects become the property of the family.

Another option is to sell granny squares so that the money received can be used as a down payment along with maternal capital.

In this case, permission from the guardianship authorities is issued, since we are talking about depriving children of a share of the inheritance.

How to allocate a share in a mortgaged apartment to a child?

Instant transfer of a share is most often impossible. This fact is due to the fact that the square meters belong to the bank until the mortgage is repaid. An alternative is to formalize a deferred execution, issued if maternity capital was used. After the debt is repaid, the share is transferred on the basis of a gift or by mutual consent of the parents. Another possibility is to register a share through the court.

Procedure, instructions

Proper implementation of the procedure for allocating shares is a guarantee of providing the offspring with housing. The step-by-step instructions suggest:

- Submitting an application for mortgage lending from Sberbank.

- Obtaining approval from Sberbank with consent to allocate a share.

- Discussion of loan terms (term, amount, interest rate).

- Providing Sberbank's consent to the guardianship authorities.

- Signing a real estate purchase and sale agreement.

- Registration of the allocation of the children's share in the total volume of the quadrature.

- Sign a loan agreement for the purchase of housing with Sberbank.

- Pay off your mortgage in full without delays.

The difficulty is that each step is associated with a number of difficulties that you have to go through. A large number of authorities and documents, approvals, justification, etc. But any problem can be solved if you follow the above instructions.

Required documents

To approach the procedure prepared, you must do the following:

- Get an opinion on the value of the property.

- Obtain a receipt from the owner of the property that the apartment is ready for re-registration.

- Provide written consent from the spouses.

- Receive an extract from the Unified State Register of Real Estate (USRN).

- Prepare a certificate of employment (copy of the work book, license to operate an individual entrepreneur, copy of the employment contract, certificate 2-NDFL, etc.).

- Marriage certificate.

Cadastral papers are not provided. Rosreestr requests data independently. And to get a statement for Sberbank, you will have to prepare:

- identification documents of all participants in the allocation of shares;

- marriage certificate (original and copy);

- receipt for payment of state duty;

- child's birth certificate;

- papers proving the right to own housing;

- written consent of the baby's father and mother.

All papers must be valid. The list is long, but as a rule, every borrower has documentation.

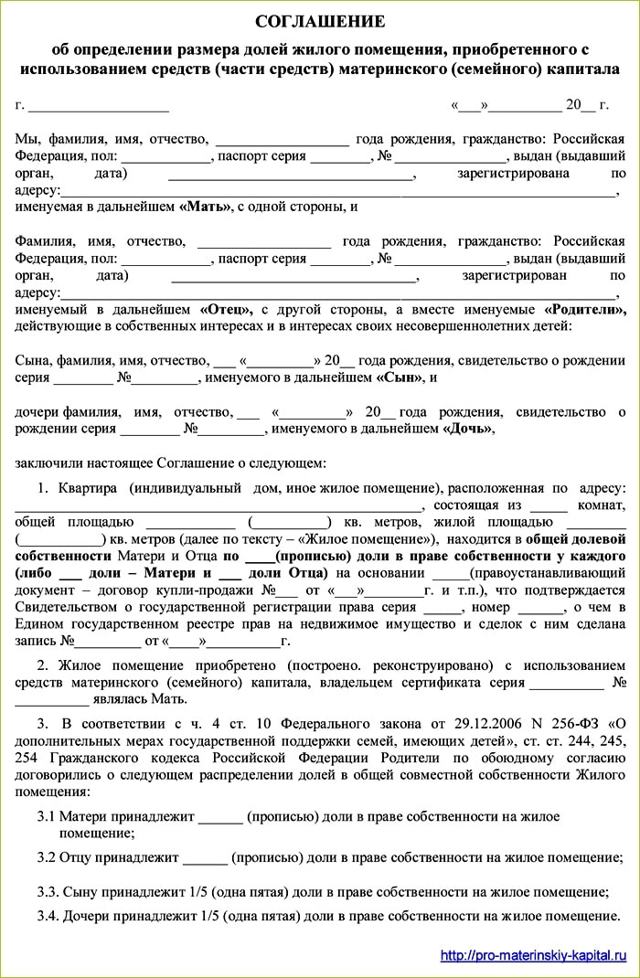

Agreement on allocating a share to children

At its core, this document is an obligation assumed by parents. Controls the transfer of the share to the Pension Fund of the Russian Federation if maternity capital is used. A special feature of the design is mandatory notarization. Obligations come into force from the moment the mortgage agreement is signed at Sberbank.

The child is allocated a share no less than that specified in the legislative acts of Russia. For regions, the number of square meters varies. The average required area is 12 sq.m. the document does not have a unified form, but this is rather a minus. You must provide all required information. A sample parental agreement for the allocation of a share can be downloaded on the Internet or obtained from a notary.

Deadlines

The situation here has a number of features. Each case with regard to the timing of determining the share is individual. It all depends on the following factors:

- Sberbank approval is issued within a period of ten to one month.

- It takes up to two weeks to obtain permission from the guardianship authorities.

- The period allotted for the execution of the agreement is up to six months.

- Registration with Rosreestr will take from 14 to 30 days.

The trial is carried out within 2-6 months, if there are no complications. At the same time, the procedure involves expenses, and this is in addition to the obligation to repay the debt to Sberbank.

Cost, expenses

Together with notarization, the agreement or obligation will cost from 300 to 20,000 rubles. If registration is made not through Sberbank but through the court, the state fee for filing an application depends on the value of the claim and is calculated personally. Other certificates will also require expenses. Half tires range from 100 to 1000 rubles.

Useful tips

Before implementing the decision, the child must complete preliminary documents. The feasibility of providing existing housing as collateral is assessed. If consent cannot be obtained, you can proceed through the court. Sberbank consultants are ready to provide legal support. Consultation is available by phone, in person or online.

The procedure for allocating a share to children in an apartment purchased using maternity capital

We propose to consider the topic: “the procedure for allocating a share to children in an apartment purchased with maternity capital” with comments from professionals. We tried to explain everything in understandable languages and fully cover the topic. Read the article carefully and if you have any questions, you can ask them in the comments or directly to the consultant on duty.

According to Law No. 256-FZ of December 29, 2006

on additional measures of state support for families, if maternal capital is used to improve housing conditions, then the spouses are obliged to allocate shares in the housing purchased, built or reconstructed with their funds to themselves and all children, including those who will be born or adopted subsequently. If the certificate funds compensate for construction or reconstruction, and the living space is in common joint or individual ownership, then the shares are also allocated.

When submitting an application for disposal to the Pension Fund, it is also necessary to provide a notarized obligation to allocate shares.

The shares are distributed among family members within six months after the conditions specified in the obligation are met.

The cost of preparing this document is not determined by law - the notary sets it independently .

The allocation of shares in housing that is purchased (built, reconstructed) with maternity capital, as a rule, is certified by a notary (with the exception of some cases). If the share is transferred under a gift agreement, then the state duty will be 0.5% of the assessed value of the housing

Banks offer to legalize mortgage refinancing with capital

The Association of Russian Banks (ARB) proposed legislatively allowing the refinancing of mortgage loans for which maternity capital was used to obtain or partially repay.

ARB sent a letter to State Duma Speaker Vyacheslav Volodin with a bill that changes the procedure for registering shared ownership of children.

In particular, it allows the allocation of shares to minor children after full repayment of the loan, including refinanced ones.

It is expected that this will allow families with children to seriously save on their mortgage.

If now the weighted average rate on housing loans is 9.52 percent per annum (according to the Central Bank as of November 2018), then 3-4 years ago it rarely fell below 12.5 percent, and on average rates fluctuated in the range of 13-15 percent.

People who took out a mortgage in 2014-2016 and used maternity capital would be happy to reduce the rate now, but often cannot refinance.

Matkapital will be issued to families who received Russian citizenship after the birth of children.

After the loan is fully repaid - this occurs automatically upon refinancing - and the collateral is removed, the borrower is obliged to register shares in the property for the spouse and children, including minors, within six months. It would seem that there is no problem here, but it arises when the question arises of transferring a minor’s share as collateral to the bank.

This requires permission from the guardianship and trusteeship authorities. But they often refuse to issue it due to the risk of losing the child’s property in the event of foreclosure on his share, the ARB emphasizes. “When refinancing, the collateral under the original loan agreement is removed, which means there is a need to allocate shares to the children.

But the guardianship and trusteeship authorities do not give their consent to the transfer of the apartment as collateral under the new agreement, and banks do not want to provide loans without collateral.

Families cannot refinance their mortgage and improve their financial situation due to the imperfection of the legislative framework,” says Andrey Andreev, managing partner of the U&Partners law office.

In addition, documents for removing the encumbrance and imposing a new one are submitted to the MFC at the same time. In fact, the apartment is in an unsecured position for less than a day. And as soon as the encumbrance is registered, the bank that refinanced the mortgage refuses to allocate shares to the children in the mortgaged property.

“Formally, it is possible to refinance a mortgage loan, for the partial repayment of which maternity capital was used,” notes Evgeny Pugachev, lawyer at the Intellectual Capital law firm.

“But if the shares are not allocated to all family members, the bank will most likely refuse due to the risk of challenging the collateral transaction.

If the shares are allocated, then the bank is not interested in refinancing the loan, since it will receive an apartment with minor owners as collateral, which greatly complicates the foreclosure of the collateral and increases the level of risk.”

Applications for the issuance of maternity capital will be considered twice as fast

ARB proposes to register the rights of all family members to the apartment only after the mortgage has been repaid in full from the last creditor. This will allow families to refinance loans and reduce the cost of servicing them without fear of being subject to sanctions.

In addition, the ARB proposes to introduce control over the registration of a share in the ownership of a child’s residential premises at the legislative level. This will make the real estate market more transparent and reduce the incidence of abuse when children are not allocated their due shares.

Many borrowers, in an attempt to reduce the interest on the loan, are forced to violate the obligation to register shares in the ownership of the real estate of all family members after the encumbrance is removed. The consequences of such behavior can be challenged both by the prosecutor's office and by the child himself upon reaching 18 years of age.

“Now the allocation of shares in the right to housing, for the acquisition of which maternal capital was used, is almost not monitored,” adds Pugachev. “But if it is established that such an apartment was sold without allocating shares to all family members, the sale transaction may be declared invalid.”

You may be allowed to register shares for children after the mortgage has been fully repaid from the last lender.

According to the head of the State Duma Committee on the Financial Market, Anatoly Aksakov, the initiative is being discussed with might and main in the State Duma, and there is a chance of its consideration already in the spring session.

How to allocate shares to children in a mortgaged apartment

100 lawyers are now on the site

- Good afternoon

- I ask for your advice:

- In March 2016, my wife and I completely repaid the AHML mortgage on our one-room apartment ahead of schedule.

- In 15, we received and used a maternity certificate to partially repay our one-room apartment.

- In 1515, the Pension Fund obliged us to draw up an obligation with a notary to allocate shares to children in our one-room apartment.

- But, I now plan to put our one-room apartment up for sale (+ it is necessary to pick up the mortgage and remove the encumbrance).

- In parallel, during March 16, I plan to buy a new ready-made two-room apartment with a new mortgage, without waiting for the sale of my one-room apartment.

Question: Can we allocate shares under the obligation to our children in a new, ready-to-purchase two-room apartment that is larger in area? I have no desire to allocate space in my one-room apartment, which will soon be sold. I assume an obstacle from the state registry, the pension fund and the bank of the mortgage holder for the newly acquired two-room apartment.

- I actually don’t want to break the law, I plan to allocate even a larger share, but the obligation states in black and white that shares should be allocated strictly in an old one-room apartment.

- We are confused, what to do?

- Thank you in advance!

- Sincerely,

- Karmadonov Grigory

- 8-905-647-70-15

Client clarification

If you still allocate shares in the new two-room apartment, will the mortgagee bank (Sberbank) give its consent?

And there is an opinion whether it has the right to life:

“If you bought one apartment with a mortgage, and you want to allocate the obligatory shares to the children in another, try to complete the transaction so that both housing is in your property at the same time and at this moment apply for permission from the guardianship department. In this case, you should not refuse to allocate shares to children in an apartment with a large area, even if it is not indicated in the obligation.”

Client clarification

- Good afternoon

- I contacted Sberbank and they told me that shares could be allocated to children.

- You need to contact the guardianship department and they give their consent, we accept it and issue a mortgage with the allocation of shares in the new mortgaged two-room apartment.

- She said the practice is standard, there is nothing surprising, many people use it.

Client clarification

Good morning!

New information, when contacting the territorial guardianship and trusteeship authority of Yaroslavl, the following response was received:

We will not give consent, because... By your obligation, you must allocate shares in the one-room apartment, and only there. They said go to the pension fund and resolve the issue of replacing the item (apartment) to be allocated.

Yesterday the bank meant that, in principle, it would allocate shares in a new apartment purchased on credit. But if we have an obligation to the old one, then nothing can help.

Actually something like this.

Client clarification

- Question to the bank:

- If we now buy an apartment with a mortgage without allocating shares to the children, and we allocate these same shares in our apartment under a notarial obligation, is it possible later (before the end of 2016) when selling our old apartment with shares already allocated, to re-allocate shares in the new one we have already purchased? apartments using Sberbank funds and held as collateral by you?

- I ask this because when selling your old apartment, it is necessary to allocate shares somewhere that are no worse than they were.

- Bank response:

- Yes, sure.

Client clarification

- Good afternoon

- The decision was made to close the mortgage on the old apartment and not sell it.

- Calmly allocate shares and live for some time during this crisis period in the country without a single loan or debt.

- Thanks EVERYONE!

Online legal consultation Response on the website within 15 minutes Ask a question

Answers from lawyers (7)

Hello, Gregory.

Can we allocate shares under the obligation to our children in a new ready-to-purchase two-room apartment, larger in area? Gregory

By law, of course, you must allocate shares in the apartment that is indicated in the obligation. But since the other apartment will be larger in area and you will allocate shares to the children in this apartment, this will not be a violation of the rights of children. It will not be a deterioration of their living conditions.

I assume an obstacle from the state registry, the pension fund and the bank of the mortgage holder for the newly acquired two-room apartment. Gregory

If the encumbrance has been removed from a one-room apartment, then Rosreestr and the Pension Fund of the Russian Federation cannot in any way prevent you from selling it. The fact that you have not allocated shares in the apartment does not interest these structures.

- 10.0 rating

- 4665 reviews

- expert

Question: Can we allocate shares under the obligation to our children in a new, ready-to-purchase two-room apartment that is larger in area? I have no desire to allocate space in my one-room apartment, which will soon be sold. I assume an obstacle from the state registry, the pension fund and the bank of the mortgage holder for the newly acquired two-room apartment. Gregory

Good afternoon.

I still believe that there may be difficulties, since the obligation was given to allocate shares in a one-room apartment. And this obligation must be fulfilled exactly in the form in which it was given.

That fact. that the new apartment no longer violates the rights of the rest of the family, of course, but this still needs to be justified and it is not a fact that anyone will want to go into this.

You can try, but I think it will be problematic since the approach here is quite formal.

At the same time, if no one complains anywhere, then everything may well pass.

With respect. Vasiliev Dmitry.

Hello. You can try to rewrite the obligation to another living space. To do this, contact the Pension Fund authorities. Since there will be no infringement of the rights of minors, I think the Pension Fund will not object

Good afternoon

Formally, the scheme should be like this - first you allocate shares in a one-room apartment, then, in order to sell it, you must obtain the consent of the guardianship authorities and provide them with evidence that the rights of the children will not be violated and they will be provided with housing no worse.

But, if you sell a one-room apartment, but at the same time allocate shares in a two-room apartment, then there should be no problems later. Since the rights of children will not be violated in the end, there can be no liability for violation of a notarial obligation.

I actually don’t want to break the law, I plan to allocate even a larger share, but the obligation states in black and white that shares should be allocated strictly in an old one-room apartment. We are confused, what to do? Gregory

Gregory, you need to contact the guardianship authorities, because their job is to monitor the provision of minors. I assume their answer is that the only option is to wait for the property, allocate shares and sell with the permission of the guardianship while simultaneously purchasing another apartment. Because this is a legal option.

But if the future apartment has better comfort and a better location, then they may be allowed to transfer the obligation to a new home. You need to simply convince the guardianship authorities that the new home is better in all respects. For example: the school is closer, the infrastructure is better, etc.

I actually don’t want to break the law, I plan to allocate even a larger share, but the obligation states in black and white that shares should be allocated strictly in an old one-room apartment . Grigory

Hello!

We are confused, what to do? Gregory

Allocate in a one-room apartment, then sell with the prior permission of the guardianship authorities.

I assume an obstacle from the state registry, the pension fund and the bank of the mortgage holder for the newly acquired two-room apartment. Gregory

What are the obstacles?

Can we allocate shares under the obligation to our children in a new ready-to-purchase two-room apartment, larger in area? Gregory

Good afternoon I recommend not to go this route - since you have a written obligation for a property purchased using maternity capital funds.

Then problems may simply arise and the transaction may be challenged in the court of the Pension Fund of the Russian Federation that issued the MK.

It is better to first allocate the shares as indicated in the written commitment and, with peace of mind, resolve the issue of purchasing housing further.

I have no desire to allocate space in my one-room apartment, which will soon be sold. I assume an obstacle from the state registry, the pension fund and the bank of the mortgage holder for the newly acquired two-room apartment. Gregory

This is understandable - a lot of time and nerves - but what to do.

We are confused, what to do? Gregory

In this case, I recommend: 1. Go to the Pension Fund and inquire about this issue in the department for working with MK funds - they will tell you what to do and inform you about the possible legal consequences. 2.

Go to the guardianship and trusteeship authorities regarding the issue of obtaining permission to alienate residential space (in which the children will be the shared owners after allocating shares to them) in order to acquire a larger area - they will also tell you what they need to submit in order to issue you a written permission. Sincerely…

Is it possible to allocate a share to a child in a mortgaged apartment?

For young families who purchased an apartment with borrowed funds, in certain situations it is important to know in advance whether it is possible to allocate a share to a child in the mortgaged apartment. Sometimes it depends on whether they can move to more comfortable housing.

The problem of allocating shares to children in mortgaged housing

If the apartment was purchased with a mortgage, and maternity capital funds were used to repay part of the debt, then allocating a share to children in such housing is mandatory. This is one of the conditions for using this preference.

Usually, first a mortgage agreement is concluded, real estate is purchased, and only then families are faced with the problem of having to comply with the requirements of the law. Even if the right to maternity capital funds arose before the sale and purchase transaction, children are still not indicated in such documents as future homeowners.

Real estate transactions involving minors, in cases where the property is pledged, are carried out exclusively with the consent of the guardianship authorities.

If initially we are talking about the sale of housing in which there is a share of a minor, with the aim of purchasing another property using mortgage funds, then it is better to immediately indicate in the application for a mortgage, and subsequently in the purchase and sale agreement, that it will become one of the owners. Then you need to obtain consent from the guardianship authorities to sell the minor’s share in the existing housing and to pledge his share in the new one. There may be problems with the latter, because there is a risk of non-payment of the mortgage. Then the minor will be left without housing at all.

When making such a transaction, the living conditions of the children should not worsen. Guardianship looks at both the quality of both real estate objects and the actual size of the share (essentially the area) that already belongs and is expected to belong to the minor.

If the child is over 14 years old, his consent will be required to complete the purchase and sale transaction and subsequent mortgage.

Solving the problem of allocating shares to children in mortgaged housing

Allocation of a share to a child in a mortgaged apartment is possible if two conditions are simultaneously met:

- consent of the guardianship authorities that the property of the minor will be pledged;

- the creditor's consent to formalize the allocation of a share to the child.

Banks are in no hurry to meet clients halfway and give their consent to the allocation of shares to minors.

And this despite the fact that if there is permission for the transaction from the guardianship authorities, if problems arise with payments, the rights of the creditor are protected by law.

The bank can sell the pledged property based on a court decision, even if the share in it is the property of a minor, and thus compensate for its losses.

If we are talking about the use of maternity capital funds, the Pension Fund asks to bring a notarized promise to provide shares in the purchased residential real estate to children after repaying the loan and removing the encumbrance. The problem can also be resolved in court, that is, by obliging the lender, on the basis of a court decision, to give its consent to the allocation of a share in the mortgaged housing to children.

In the event of a sale of a share and the need to buy a new home with a mortgage, as a rule, they look for a way out by giving the child a share in another property, for example, in a grandparent’s apartment.